Table of Content

While home insurance companies offer endorsements that can fill in coverage gaps, people with high-value homes could still be left significantly underinsured. Homeowners insurance rates are impacted by age and size of the home, claim history, cost of construction materials, and also by location. Read on to compare home insurance rates by insurance company, state – even down to ZIP code – and find out what you can expect to pay for the coverage you need. The average home insurance cost is $2,777 per year nationwide for a policy with $300,000 in dwelling coverage and liability and a $1,000 deductible, based on 2022 Insurance.com data. AIG’s Private Client high-value home insurance policy fully addresses your exclusive insurance needs.

Its average annual rate is 61% higher than the national average home insurance cost. High-value home insurance policies generally include replacement cost automatically. They also typically provide higher coverage limits for valuable items such as jewelry. If you compare standard insurance policies from broad-market companies, beneath the marketing slogans, you’ll find many policies are similar. Often, they share the same limitations, capping coverage limits for homes and personal liability insurance.

Compare home insurance rates

A higher dwelling coverage typically results in higher annual premium, but it’s still possible to find competitive premiums from different home insurance carriers. The proprietary rate data below highlights how your dwelling coverage limit could affect your average homeowners premium. An umbrella policy with $5M limits can cost about $1,500 annually.

Your total insured value for your home is now $3.4 million, giving you an estimated insurance cost of $6,120 per year. Some insurers can only offer limited or inadequate coverage and may not have an available package for a house that costs one million or more. It is a must to learn specialty coverage to protect your million-dollar house from unfortunate circumstances. Unlike standard coverages, specialty coverages have adjustable policies that will give you options on how much coverage you prefer.

Get Home Insurance for a 1 Million Dollar House!

This rough estimate is necessary to make your house good as new after any possible repair and restoration that you may need in the future. The cost of insuring a multi-million-dollar house is different from that of a place insured for a higher value. We’ve analyzed pricing data from 150 insurance companies to bring you the average homeowners insurance cost in every state and the largest U.S. cities. You may see premium increases at your policy renewal even when you haven’t changed your coverage. Insurance companies often adjust your coverage limits to keep pace with inflation, which helps to ensure your home is still properly covered when things get more expensive.

Our sample policy includes $300,000 of dwelling coverage, $300,000 of liability coverage and a $1,000 deductible. The cost of your own homeowners insurance will depend on your location, the size of your house and how much coverage you need. Each homeowners insurance company sets its rates, which means that the average home insurance cost will vary from carrier to carrier even within the same state and ZIP code .

Average homeowners insurance cost by home age

So, how much should you budget for homeowners insurance in these locations? These states have average premiums that are less than $1,000 per year, likely due to a relatively low risk of home damage from natural disasters like tornadoes, hurricanes and wildfires. Below, you can see the average cost of home insurance coverage in these states and how the prices compare to the national average. Our analysis of average homeowners insurance rates by state found that Hawaii is the cheapest state for homeowners insurance at an average of $558. On the other end of the spectrum is Oklahoma, which has an average annual rate of $4,122. The $3,564 difference in costs shows that a home’s location really does matter.

The easiest and most effective way to find an affordable home insurance policy that is customized for you is by using Jerry. Corporations and Non-Government Organizations can purchase kidnap and ransom coverage to protect their employees and volunteers from the effects of kidnapping and ransom demands. If you travel to countries in which the U.S. has an active travel ban, such as Syria or Iran, your coverage will be considered null and void. Specialty coverages will suit and be a perfect addition to each of your coverage, depending on your risk profile. Crime statistics in your area are also considered for loss assessment.

Step 2: Decide how much homeowners liability you need (and medical payments)

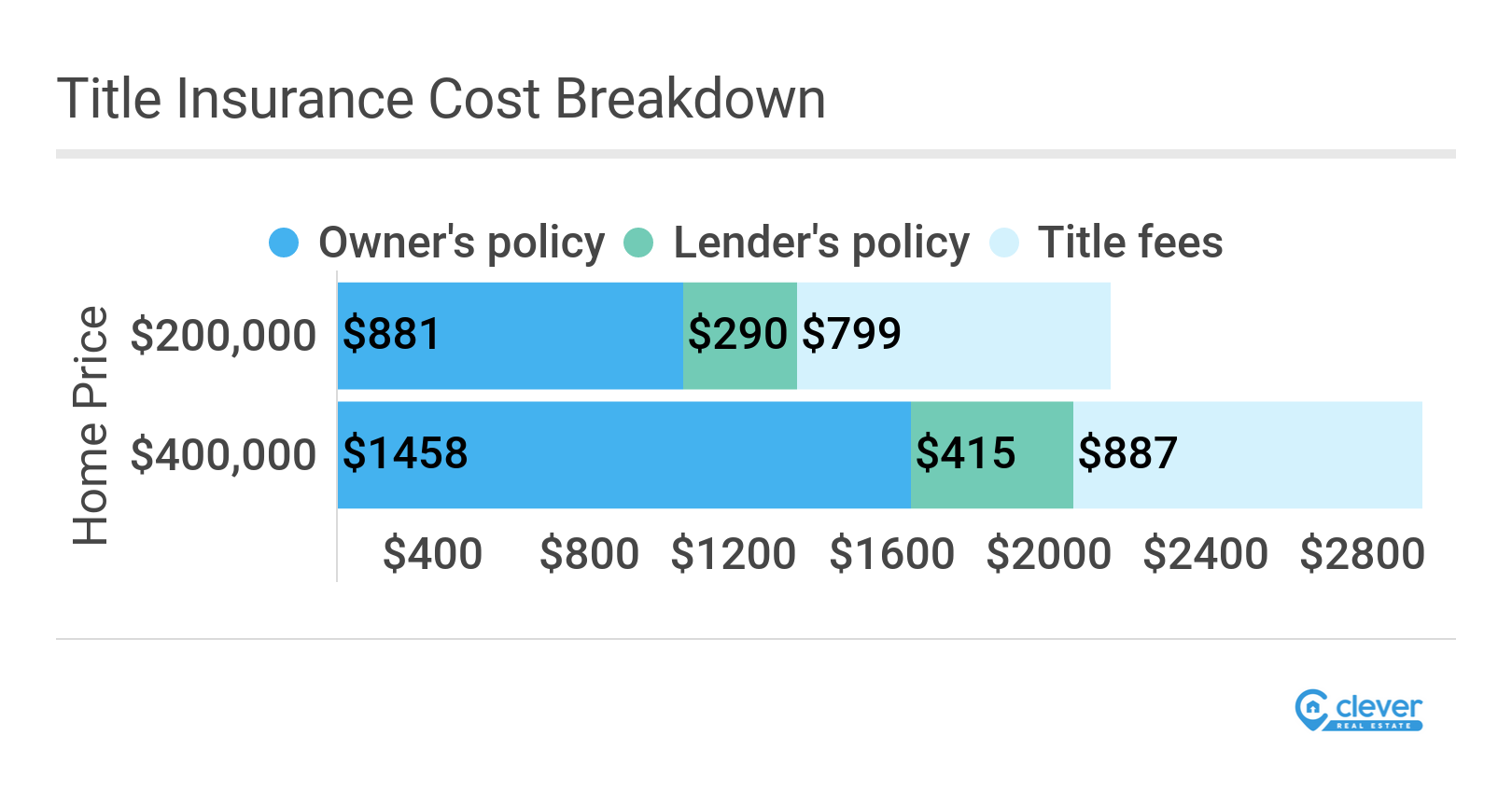

Every year, you should review your homeowners insurance, including your liability coverage, premium, and deductible. Guaranteed replacement cost coverage allows you to replace or rebuild your house, even if the damage is beyond your policy’s limits. You should know both market value and replacement cost since the coverage only applies to rebuilding your house at the same spot. A million-dollar house uses a formulaic rate to estimate the cost of home insurance.

If you file a claim during your policy term, you could see an increase in your premium at your renewal. Depending on the severity of your claim, the cause of the damage and the underlying factors on your policy, you may see anywhere from a modest to a substantial increase in premium after a claim. Not every homeowners insurance policy contains the same components. If you are unsure what your policy covers, talk to your agent or insurance company for clarification. In addition to the state you live in, your individual city may also have an impact on your home insurance rates.

Whether your home is valued at $1 million, $2 million, $3 million, $5 million, or even $10 million or more, multimillion-dollar homes come with a unique set of coverage considerations. To determine how much you’ll pay for home insurance, contact a few insurance companies by calling to chat with an agent or by filling out a form on their website. After you share some information about you and your home, they’ll run this information through their own algorithms to come up with a quote on how much your insurance will cost. Pure offers you the option to receive a claim settlement in cash, protection coverage up to $50,000 for jewelry, drain backup coverage, and replacement of damaged items at present-day cost. Additionally, a single dedicated adjuster – PURE Member Advocate will be available to assist you with temporary housing and introduction to local contractors and vendors.

Being licensed from the Department of Financial Services, Experienced Public Adjusters are professionals who advise and manage claims on behalf of policyholders so we understand your needs. The coverage for temporary housing, including any additional living expenses, is provided for by Loss of Use coverage. This coverage is relevant when your house is being repaired or rebuilt. Some carriers limit the time they can shoulder, while others insurance providers have unlimited coverage. If you rent out your property, the loss of use coverage helps cover the lost rent if your tenant has to move out because of the property loss. Home insurance for million dollar homes can have other valuables included.

The deductible is your share of the repair cost when you file a claim. Your home insurance premium will be lower if you choose a high deductible. If you have a $500 deductible, you're going to pay more on your premiums than if you have a $2,000 deductible. The cost to insure a million-dollar home will vary a great deal based on location, the individual characteristics of each home and the unique needs of the homeowner. While $0.18 per $100 is a common range in areas like Nassau County, New York, some insurers offer an additional discount for LEEDS-certified construction.

You can choose between these various insurance levels based on your personal comfort level, tolerance for risk, and how much money you have in the bank in case of emergencies. “Open perils policies provide the strongest protection, because they cover all possible causes of loss except for those that are specifically excluded,” he notes. You can lower your rates by adding storm shutters, updating your roof, and other risk-mitigating changes. You should also consider streamlining the heating system, electrical system, and plumbing in order to lower the possibility of fire and water damage. Nearly all states allow insurers to consider a person's credit history. The claims history includes both claims you filed and ones that previous owners filed.

No comments:

Post a Comment